11 March 2026

The Hardware Side Of Offline Biometric KYC

Fingerprint-based Aadhaar KYC is only as good as the device behind it. Here's what NBFCs and lenders need to know.

11 March 2026

Fingerprint-based Aadhaar KYC is only as good as the device behind it. Here's what NBFCs and lenders need to know.

India's lending landscape has changed dramatically over the last decade. NBFCs, microfinance institutions, and cooperative banks are now reaching borrowers in places where a branch never existed and they're onboarding them on the spot, with nothing more than an Aadhaar number and a fingerprint.

Offline e-KYC using biometric authentication has made this possible. But in the rush to digitise onboarding workflows, one question consistently gets less attention than it deserves: what's the device actually doing the verification, and is it up to the job?

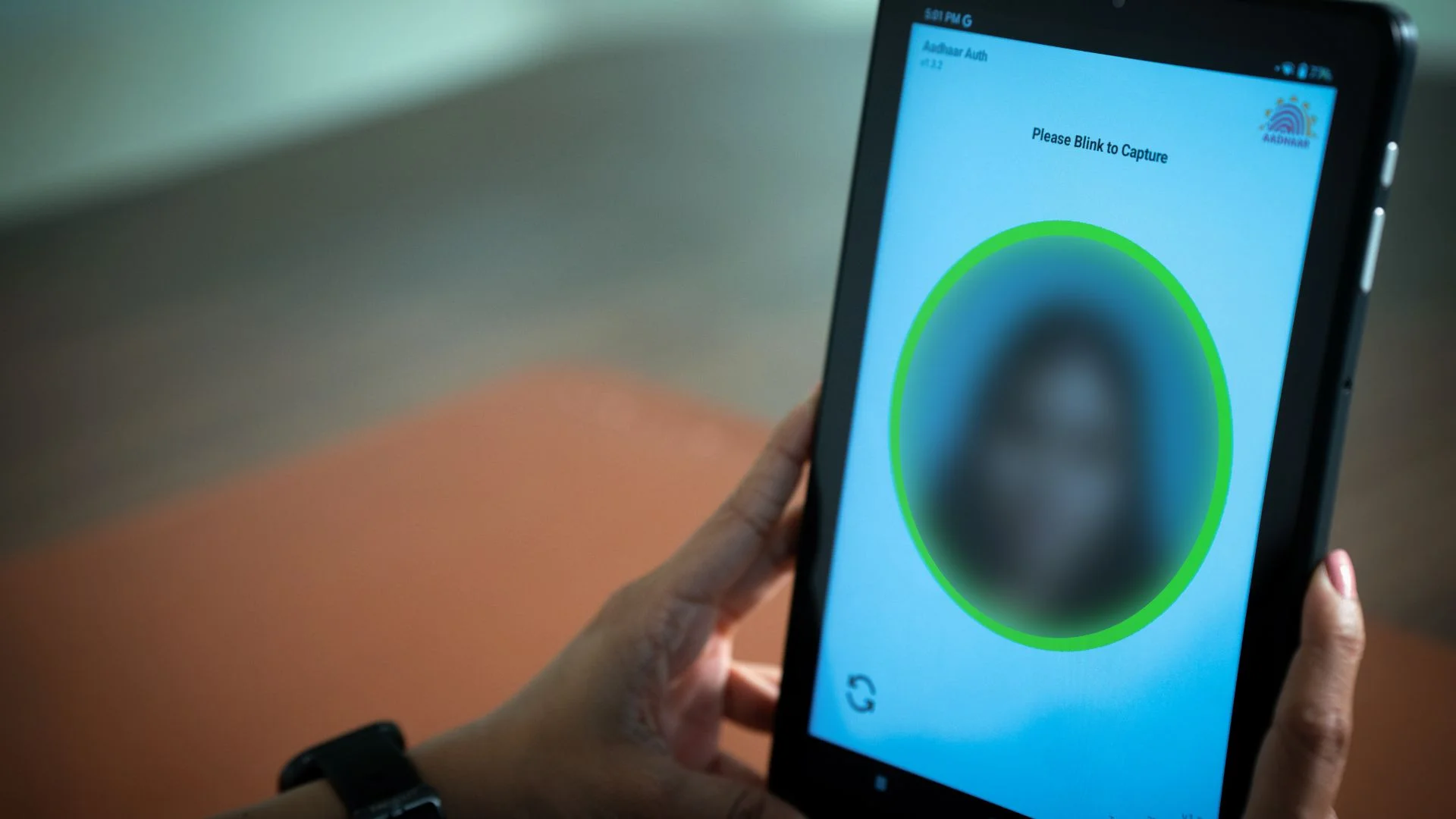

When a field agent from an NBFC visits a borrower in a semi-urban locality to process a loan application, the KYC process works like this: the applicant provides their Aadhaar number, places their finger on a biometric sensor, and the device captures and encrypts that fingerprint locally before sending an authentication request to UIDAI. No internet-dependent data transfer of raw biometric data. No storing of sensitive information on the device. The authentication either confirms or doesn't.

This is the elegance of the offline model. It removes the need for physical document verification, eliminates the risk of forged paperwork, and compresses what used to be a multi-day onboarding process into minutes.

But that entire chain of trust starts at the sensor. If the capture is poor, the authentication fails. If the device isn't certified, the transaction isn't valid. If the encryption doesn't happen at the hardware level, the process isn't compliant.

Most discussions about e-KYC in the NBFC and fintech space centre around the software stack, the KYC platform, the API integration, the data storage architecture. The device is often treated as a commodity, something to procure at the lowest available price point.

That assumption gets expensive quickly.

Field KYC deployments face the same challenges as BC banking such as calloused fingers, outdoor conditions, and inconsistent surfaces, but with an added layer of consequence. A failed authentication during loan onboarding doesn't just inconvenience the customer. It delays disbursement, increases the cost of the field visit, and in competitive lending markets, it can cost you the customer entirely.

Beyond failure rates, there's a compliance dimension. UIDAI mandates L1-certified devices for Aadhaar authentication, which means the fingerprint must be encrypted on the device itself, using a secure element, before it ever leaves the sensor. A device that doesn't meet this standard isn't just operationally unreliable. It isn't legally usable for Aadhaar-based KYC at all.

For an NBFC's compliance and operations team, L1 certification is worth understanding beyond the acronym.

An L1-certified device has a secure processing environment built into the hardware, it captures the biometric, encrypts it within the device using keys that cannot be extracted, and only then transmits the encrypted data for authentication. There is no point in the process where raw biometric data is exposed.

This matters for RBI audit trails, for data protection compliance under the DPDP Act, and for the NBFC's own liability position. If a KYC authentication is ever challenged, by a borrower, a regulator, or in a fraud investigation, the integrity of the capture device is part of what establishes the authenticity of the record.

The FM220U L1 is built around exactly this architecture. It's a workhorse for high-volume authentication environments and it holds up in the kind of repeated daily use that field KYC operations demand.

Fixed-counter KYC such as at a branch or a service centre, and field KYC are different operational problems, and they benefit from different hardware approaches.

At a fixed counter, a wired device makes sense. It's stable, always charged, and easy to integrate with a desktop or kiosk setup. The A20 FP handles this well, it's built for Aadhaar authentication at the point of service, with ergonomic design that naturally guides finger placement, which quietly but meaningfully reduces failed captures in a high-footfall environment.

For field agents doing doorstep KYC, the calculus shifts. The agent is working from a phone or tablet, moving between locations, often without a stable surface or a power source. Here, a Bluetooth-enabled sensor that pairs with a mobile device is the practical answer, it removes the dependency on a laptop or fixed terminal without compromising on certification or capture quality.

Getting this distinction right at the procurement stage, rather than deploying a one-size-fits-all device across both contexts, is one of the simpler operational improvements that makes a measurable difference in field authentication success rates.

KYC platform providers will tell you their system is robust, scalable, and compliant. What they won't always tell you is that their platform's performance in the field is ceiling-capped by the hardware it runs on.

A strong API integration paired with a poor-quality sensor will still produce high rejection rates, frustrated field agents, and delayed onboarding. The software can only work with what the sensor gives it.

For NBFCs and lending institutions building or scaling field KYC operations, the hardware layer deserves a seat at the procurement table, not as an afterthought to the platform decision, but alongside it.

If you'd like to understand how Access Computech's L1-certified portfolio maps to your specific KYC deployment model, we're glad to have that conversation.